Peter - Cracking Markets @SystematicPeter

Systematic trader, fund manager. Web: https://t.co/Qga9clOPid Joined August 2022-

Tweets1K

-

Followers7K

-

Following91

-

Likes27

+87.1% with roughly -17% drawdown in 6 months. Markets are WILD. This is the same NDX rotational momentum strategy I trade live, but shown here without volatility targeting. And look at the distance it creates versus simply buying and holding NDX. The idea is not complicated: - Every month it ranks NDX stocks by past momentum. - Something simple like ROC(C,250). - If NDX is above MA200, it buys the top 5 momentum stocks. - Holds them for one month. - Then rotates again. That is it. Just systematic exposure to the strongest names while the index is in an uptrend. Personally, I volatility-target and cap the positions in live trading, because concentrated momentum can be brutal when it reverses. But this is the point: In strong momentum regimes, simple rotation can create serious benchmark separation. The rule itself is not the hard part. The hard part is accepting that the same logic which looks obvious after a +87% run can also look uncomfortable, concentrated and wrong while you are actually trading it.

Volatility targeting sounds boring until momentum goes vertical. I use it in my monthly rotational momentum system. In calm markets, each stock can get up to 20% of strategy capital. But when a stock becomes too volatile, the allocation gets smaller automatically. After yesterday’s rotation, my US stock momentum exposure became surprisingly small. The top NDX momentum names are now so volatile that the system allocated only roughly 1/3 of the planned capital to them. This is both good and bad. Good: If a drawdown comes after the hyper growth, the system is already de-risked. Smaller positions mean the portfolio gives less back. Bad: If the melt-up continues, the system participates with smaller size and makes less than it could have. That is the trade-off. Many traders want maximum exposure when everything is flying. I prefer to reduce size when the crowd feels most confident. Because my goal is not to squeeze every last dollar from a move. My goal is to keep the portfolio stable enough so I can keep trading the system through the ugly periods. That is why I volatility target my positions. Current stats and opened positions: crackingmarkets.com/ndx-momentum/

May was a strong month for my long US stock momentum systems. What made it interesting? It was the first live trading month for my long Donchian breakout system on US stocks that I shared here - and it caught names like $MU during a powerful momentum move. Could I have made more by simply holding MU? Yes. But that is not how I want to trade. Parabolic moves look amazing on screenshots, but nobody rings a bell before the reversal. My job is not to catch the absolute top. My job is to participate in momentum while controlling risk. That is why I split my systematic momentum approach into two layers in this crazy environment: Rotational momentum for longer-term exposure Swing breakout overlay with intraday trailing stops for risk control And no, trading MU last month was not survivorship bias. The system does not start with “let’s trade MU because it worked.” It works like this: Dynamically build a universe of stocks already showing strong movement Trade long Donchian breakouts on the top candidates Rotate when better opportunities appear May was a good reminder: You do not need to predict which stock will go parabolic. You need a process that can find momentum, enter it, manage risk, and move on when the edge shifts.

Looking at yesterday's long execution in HAL from my mean-reversion system, it reminded me how easy it is to create funny price action stories after the fact. The entry sits right on a support/resistance area, so I could make it sound very smart: price touched the level market respected support buyers defended the zone perfect timing clean reversal Nice story. But the reality is usually much simpler. Sometimes markets turn around S/R. Sometimes they slice through it like it is not there. And the same chart can be explained 10 different ways after the move already happened. This trade was not me reading the tape or seeing a magic level. It was simply a systematic mean-reversion entry triggered by a z-score function. Support may have helped. Or it may be coincidence. The important point is this: Charts are great for context. Rules are better for execution. Ex-post stories feel good. Mechanical entries keep you honest.

@AndyJScott No problem generating anything, but I prefer to compare the strategy itself with its variants.

Opening Range Breakout is one of the most cited intraday setups. I would not call it the best intraday strategy. There are definitely better edges out there. But I still think ORB is worth studying, because it is one of the cleanest ways to understand a basic intraday principle: Use the open to define a reference area. Then trade only if the market proves expansion outside that area. Just: define the price range - the high and low of the move inside the period place the breakout orders cancel the other side after the first fill know the invalidation level manage the trade mechanically flatten by the end of the day I tested a typical ORB baseline on NQ futures. Data: NQ continuous front-month 1-minute bars RTH only 2012-01-01 to 2026-05-06 both long and short one trade per day no re-entry zero fees zero slippage Rules: The first X minutes after the US cash open define the opening range. Buy-stop above OR high. Sell-stop below OR low. First fill wins. The other order is cancelled. Initial stop = opposite side of the range. Trailing stop ratchets by the OR range. Exit at stop or EOD flatten. I tested 15 min, 30 min and 60 min opening ranges. The interesting part: The faster opening ranges seem to have more meat today than they had 10+ years ago. This is not a finished trading system. It is more of a baseline to answer whether such a widely cited system as ORB could still be worth testing today. And it still looks like a decent starting framework for intraday research. The actual edge is probably in the details: volatility regime and range filters. Simple ideas are not automatically good. But simple ideas are often the best place to start serious research.

@thuys__ Because it is just a raw baseline test.

@AkshayK22860537 I do not see any particular one as the best. It is best to combine multiple.

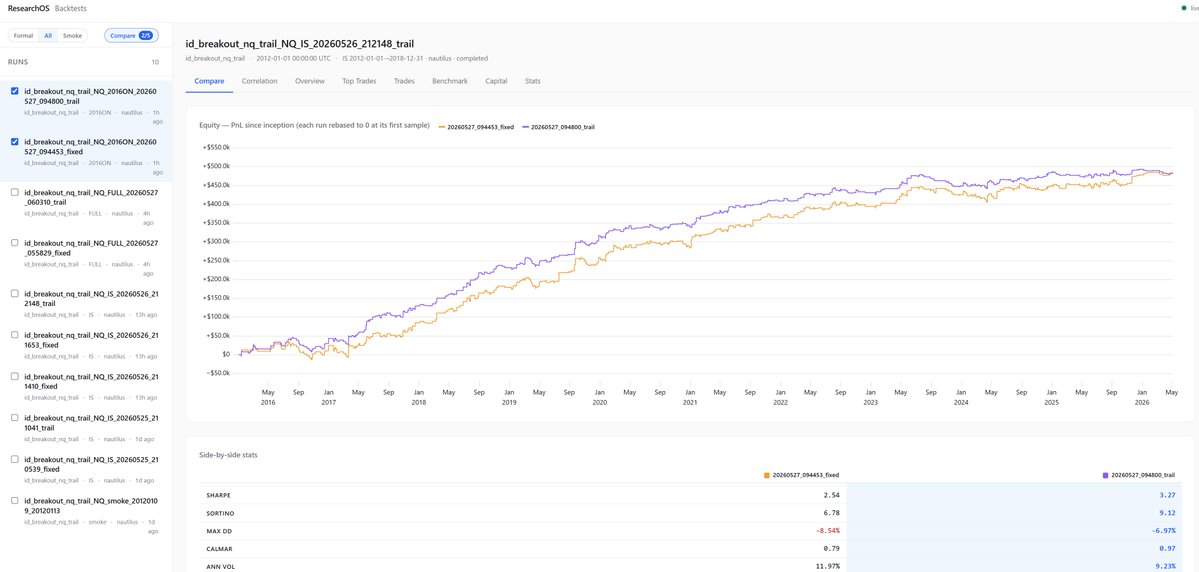

Finalizing my LLM research workflow around Nautilus Trader backtesting + Databento data. I have to say - it works better than expected. Claude Code is surprisingly good at programming Nautilus Trader. The tests are fast, clean, and I am getting far fewer annoying implementation issues than I expected. I also started building an analytical overlay on top of the backtest results, with tools for comparing backtests, showing trades, etc. And again - using an LLM makes this quite easy. Basically, it is a small research website connected to Nautilus, where I can inspect individual trades, pull up full trade info, charts, context, and compare variants quickly. Chart shows: Intraday volatility breakout on NQ (fees and slippage included). Orange - fixed SL + EOD exit Purple - trailing stop version Very easy to compare variants now.

I also tried to find the one strategy that would beat the benchmark forever. One clean logic. One simple system. One equity curve that solves everything. But in real systematic trading, that is usually the wrong goal. It is very hard to beat QQQ with a single logic, especially if you want something simple enough to have a chance to survive long term. But you do not need a home run from one system. This is a simple long mean reversion strategy I shared in full code on my blog: Sharpe > 1 Win rate around 70% Expectancy 1.17% Average exposure only 9.15% The last number is more important than most traders think. Because if a system uses only 9.15% average exposure, it leaves capital available for other systems. That means you can stack multiple simple edges instead of forcing one strategy to do all the work. This is where systematic trading starts to make sense: Not one holy grail. But a portfolio of simple, real, testable systems that use capital efficiently. You can try this one in the shared free backtester here: crackingmarkets.com/buying-short-t…

Working note from the live book: This is the long mean-reversion sleeve of my stock reversal portfolio, exported from Interactive Brokers. US + Canada stocks only. Nice run from August to March, but the last few weeks the equity curve keeps hitting the same area and not expanding. Looks like a clear resistance zone. That does not mean the edge is dead. It means this sleeve is simply not the main portfolio driver right now. Most of my current performance is coming from long momentum - especially NDX names - plus intraday breakout strategies. I am not complaining about the profits, but it is good to know where the P&L is actually coming from. This is why I like running multiple systematic sleeves. Mean reversion, momentum and intraday breakout do not need to perform at the same time. The goal is not to find one perfect system. The goal is to build a portfolio where different edges can take over in different market conditions.

Intraday trading can look excellent on paper. But the real question is not: “Is the backtest profitable?” The real question is: “How much of that profit survives live execution?” This is why I personally trade intraday slower and mostly when volatility is higher. Here is a real example from my live volatility intraday breakout trades, exported directly from Interactive Brokers. Real trades. Real fills. Real slippage. Real fees. Fees alone are eating 10.5% of gross profit. That is already close to the maximum I am personally willing to give away. Now imagine taking the same idea and making it trade much more often. The backtest may look smoother. The equity curve may look more active. The number of trades may look statistically better. But live, the cost/profit ratio can quickly move from acceptable to dangerous. This is how many profitable intraday paper strategies become losing live strategies. Not because the idea was wrong. But because the edge was too small relative to the true cost of execution. At the same time, I do not agree with the blanket statement that “intraday trading is impossible for retail after costs.” That is too simplistic. Intraday is not one category. A high-frequency strategy trading tiny edges is completely different from a slower volatility breakout strategy trading only when the market expands.

One of the biggest risks in trading is not that a simple strategy stops working. It is that the trader cannot leave it alone. My intraday volatility breakout is one of the few strategies I trade live and occasionally share in full code with others. It now has 3 years of real out-of-sample live trading behind it. And so far, the live performance is doing the main thing I really care about - behaving close enough to my prior tests. The strategy is intentionally simple. As with everything I trade, the edge is not in complexity. But when I share this strategy with others, the usual reaction is almost always the same: Can we make it trade more often? Can we smooth the equity curve? Can we remove the drawdowns? Can we add another filter? Can we improve the bad periods? I understand the temptation. But this is exactly where many traders destroy good systems. Markets are not machines that reward perfection. They reward robustness. The more energy you spend perfecting a strategy on historical data, the more likely you are fitting noise, not edge. Drawdowns are usually not a problem that needs fixing. Low trade frequency is not always a weakness. Ugly periods are not always a sign that the strategy is broken. Sometimes they are simply the cost of having an edge that can survive outside the backtest. Almost 30 years in markets taught me this: - The simplest things usually work best. - Not because they are perfect. - Because they are harder to fool. Accepting imperfections is one of the most underrated skills in trading. The equity curve on the screen is not marketing fantasy. It is the same intraday volatility breakout I live trade, with the portfolio tracked daily on my blog where you can find the full stats. $200 risk per trade, no compounding, IBKR fees applied.

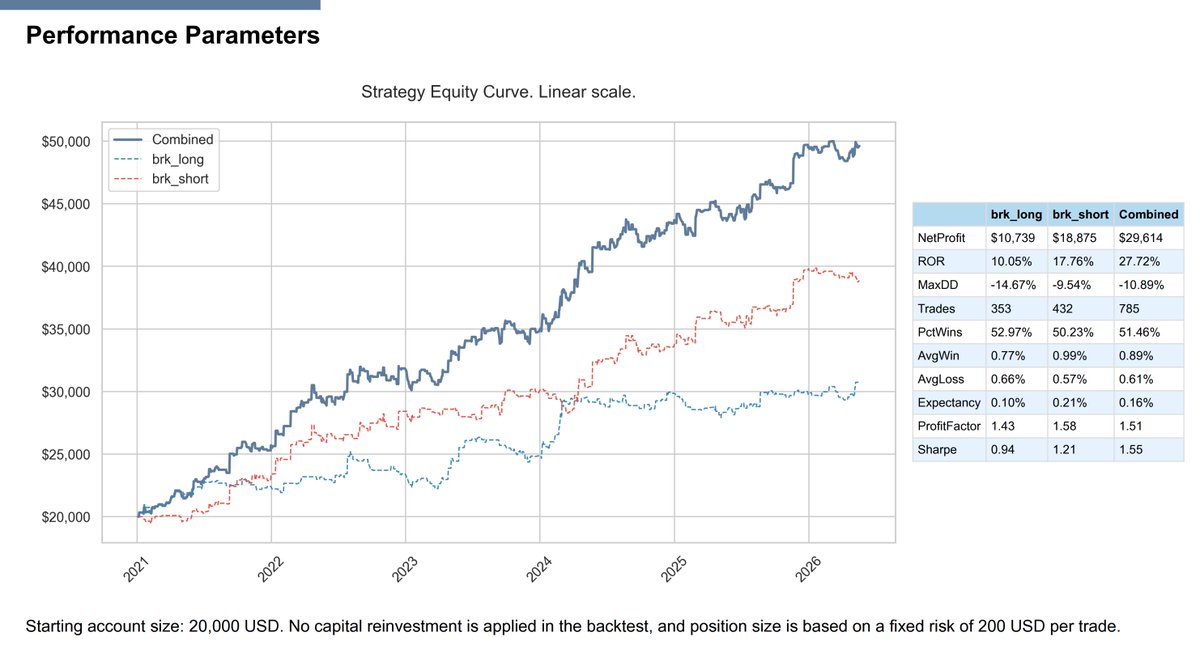

Hard to short indices in this environment. And yet, even the short leg of the volatility breakout system is still holding up. You do not need every trade to work. All it takes is being positioned correctly on the few days when the market finally expands. One strong breakout day can move the equity curve significantly. That is why the real skill is not prediction. The real skill is patience - and placing the orders when they are supposed to be in the market. The basic principle behind the idea is simple: Open as reference price If the market is volatile enough Long trigger = Open + ATR Short trigger = Open - ATR Small protective stop No trailing stop Exit at the end of day Nothing sophisticated. Just a simple volatility breakout I live trade and track publicly on my blog. Simple systems often fail because traders stop executing them before the important day arrives.

@FlowAnalyst This is really not meant to be a big team. It is just a few people I have been working with over the years.

Made quite a lot of progress with my LLM research workflow by adding Nautilus Trader + Databento. Not as “LLM hunting for the holy grail”. I, as the trader, still define the idea, market, rules, constraints and invalidation criteria. The LLM helps compress the research loop: idea -> project spec -> Databento data prep -> Nautilus backtest -> metrics + tearsheet -> red-team results -> checkpoint + git commit -> journal -> next iteration It is forcing every idea through the same process and journaling everything. Nautilus + Databento is quite powerful and can backtest in hours what would otherwise take me weeks to research. I am now comfortably running backtests of orderflow patterns, futures, stocks, options and even options strategies - including combinations with futures/stocks. Execution is not in this workflow yet. We still execute with in-house Python scripts. But for research, the speed difference is massive. What used to take me weeks can now become a structured research session. And I am especially happy that I can onboard my research team members into the same workflow, which should make everything much more efficient.

21 years with Interactive Brokers. At this point it is basically a trading marriage. I am not sure there is any other service I have used for this long.

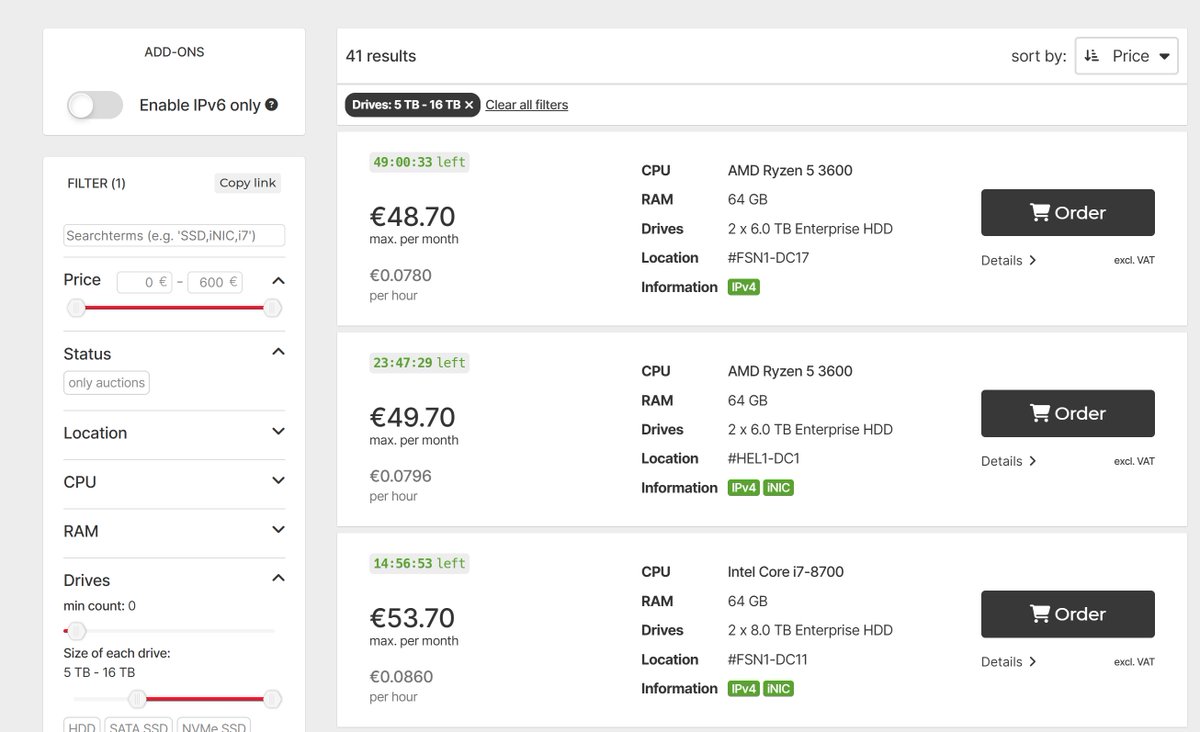

The cheapest upgrade for serious backtesting is often not a new laptop. It is renting a dedicated server. Cloud is fine, especially for short experiments. But if you work with larger historical datasets, long optimization runs, or many strategies in parallel, renting your own server can be much cheaper. I usually use Hetzner. For one of my current projects, I rented a machine with: Ryzen 7 64 GB RAM 16 TB Enterprise HDD 2 TB SSD connectivity and electricity included Price: 67.70 EUR/month. And I can cancel it any time when I no longer need it. My common workflow is simple: Claude and Codex run on the server. I connect from my notebook using PyCharm Remote Gateway. Everything feels almost local, but all heavy computation runs on the server. For systematic trading research, this is a very practical setup that scales easily and affordably. I currently have several servers running. You do not always need expensive cloud infrastructure. Sometimes the best solution is boring dedicated hardware, rented only for the months when you actually need it.

@PauloRibeiroCFA IBKR and Python. Same for equity and futures.

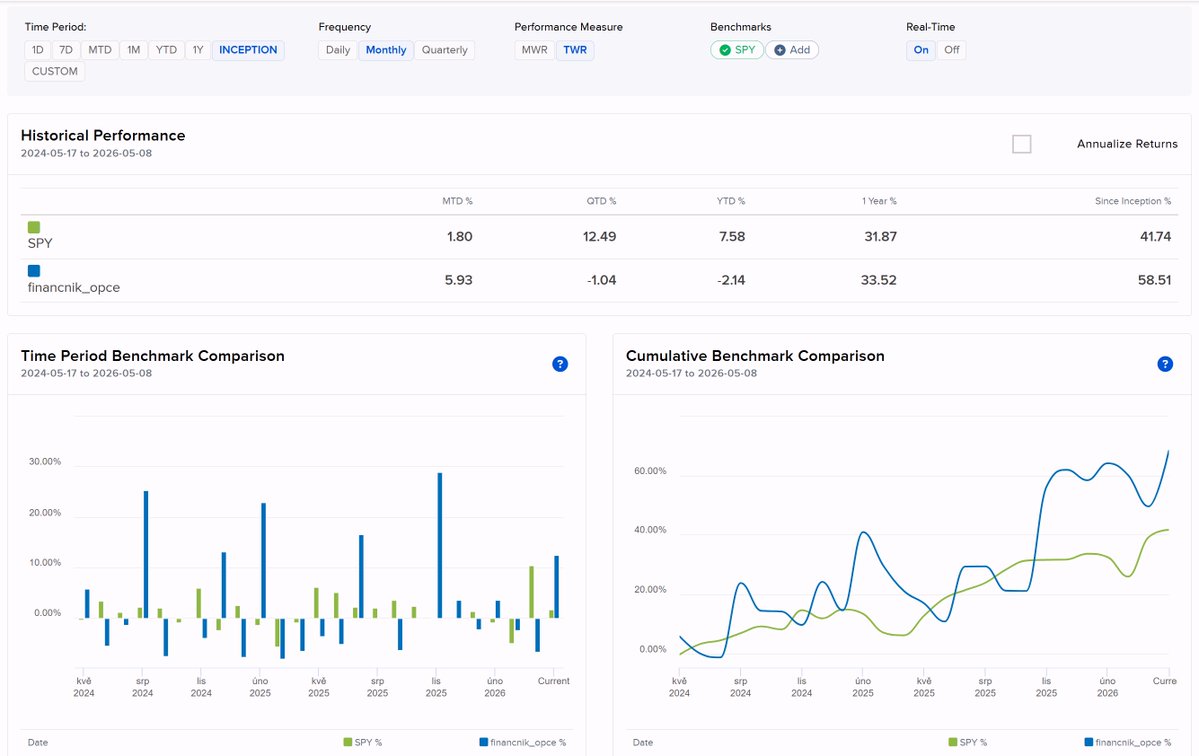

Working note from my automated long 0DTE breakout option bot: This is not the final version yet. The current bot buys ITM 0DTE options based on my volatility breakout signals. Execution is still very basic - MKT orders at the breakout - so slippage is painful. But it does not trade every day. On the contrary, it usually takes only a few trades per month. And yet, since inception: Bot: +58.5% SPY: +41.7% This is running on a smaller account and represents only the first stage of the full 0DTE automation project. Why did I start with long options? Because it was the easiest module to implement first with my current time limits. The full bot should also sell options for premium, but before combining both sides, I wanted to validate whether systematic 0DTE buying has real potential when it is tied to volatility expansion. The main lesson so far: 0DTE buying is not about being active every day. It is about waiting for the few sessions where intraday movement is large enough to overcome spread, decay, slippage, and execution costs. Most trades will lose. The equity curve will be volatile. But when the breakout is real, convexity pays. My takeaway: There is real potential in systematic 0DTE buying on SPY/QQQ when it is driven by volatility breakout logic, not random directional guessing. After validation, SPX/NDX may be even cleaner because they are cash settled. Current plan: - improve execution with limit chasing around mid instead of raw MKT orders - finish the premium selling module - solve quote database handling, because the options quote data size is currently my bottleneck

ouno @ouye46888023

2 Followers 801 Following

el jefe del flow viol... @eljefedelflou

51 Followers 613 Following

CryptoAddict @0xCrypto_Addict

53 Followers 146 Following Algorithmic trader. TradFi since 2014. Crypto since 2019. PhD in Math. Researching and implementing DeFi strategies and trading ideas. No financial advice.

Stefan @theoffer15out

34 Followers 27 Following Seasoned investor of 11 years, master of unorthodox strategies. All discussions and opinions are NOT financial advice, I love to share my muses.

Andy Hodges @Blue__Stingray

177 Followers 4K Following

DyarTrades @dy4rtrades

157 Followers 467 Following Funded trader | Eat ~ Sleep ~ Trade one setup ~ Repeat

zhobinfallah @zhobinfall29347

471 Followers 1K Following

Outsider Capital @TheOutsiderRoom

9 Followers 36 Following 8+ years in the markets. EURUSD/XAUUSD quiet performer. Watch me LIVE trade ⤵️

M T @MT47571668

417 Followers 2K Following

eseru @eseru171185

0 Followers 8 Following

karlostomy @karlostomy1

110 Followers 1K Following Do not contact me with intent to sell your courses, newsletters, or subscriptions. I may block you if you do.

Johanes | Roleta Cass... @HumildeHdr

7 Followers 58 Following 🎯 Roleta Online • HTP PRO análise real 🎥 Novo vídeo: Cavalos HTP PRO 👑 Evolua No jogo Agora! 👇 Link oficial

Dom @domjxr

8 Followers 43 Following

GoRun @GoranJ8601

1 Followers 4 Following

Ksawery MetaKowalski @KMetaKowalski

6K Followers 4K Following Piłsudczyk, już nie radykał ale ciągle patriota. PiSowski beton z braku alternatyw - sympatyk od 2005.

Obi Pascal @ObiPascal78774

0 Followers 29 Following

QNT Capital, LLC @qntcapital

1 Followers 30 Following Systematic trading and research. Risk management.

RGS Trader @rgstrading

65 Followers 327 Following

Alam J. @AlamJPhD

473 Followers 3K Following Employed as a scientist. Question everything. First principle thinking. Enjoy reading. Financial freedom. Investing/trading, business, personal finance.

.G @Ghali_J

17 Followers 1K Following

Mohit Mathur @MohitMathur01

8 Followers 142 Following

treadorBE @treadorBE

91 Followers 1K Following

dr.stone001 @Stone001Dr45346

76 Followers 3K Following

Zero Emotions @ZeroEmotionsSQX

7 Followers 33 Following We stopped working for the market and made it work for us. Automated strategies· Prop Firms · Darwinex. Powered by StrategyQuant X Unknown identity — for now

fact @3amfxct

66 Followers 39 Following

Chris Mwaura @chrismwa99

14 Followers 78 Following

Davinder Sachdeva @DavinderS49412

26 Followers 352 Following

NShenoy 🐾🐾 @shenoytech

162 Followers 2K Following Business Worker at Corporate Training Services, Enjoy sharing Humorous and Fitness tweets.

TradeSmart @Saravanan_0111

68 Followers 142 Following Son/brother/husband/Dad/IT professional/Investor/Algo Trader / Python coder Proud to be an Indian

Gel Smith @gelmyth

7 Followers 103 Following

lauora0000 @lauora000010270

43 Followers 237 Following

Tal Shilian @ShilianTal

65 Followers 1K Following

Pieter Knox @cinneesol

32 Followers 842 Following

Gaurav Ramrakhya @gfktg9

21 Followers 2K Following

Edge Del Sur @EdgeDelSur

4 Followers 57 Following Trader sistemático del sur de Buenos Aires. Documento todo el proceso.

Resenha do Malvadão @DNAdoMalvadao

9 Followers 100 Following

Wil @Wil_cx

8 Followers 199 Following

Alfred P @AlfredpFun

24 Followers 878 Following

SERSAN SISTEMAS @sersansistemas

5K Followers 672 Following 📊 25 años en trading 🤖 Sistemas en real (SYO+OYS) 📉 Sin método no hay consistencia 🎯 Empieza a automatizar ↓

Alphanume @alphanume_data

83 Followers 58 Following Alternative data APIs for people who actually trade.

Ben Trader @Tradelikeben

169 Followers 60 Following Gold Trader with Darwinex (IUJE) - Build your portfolio and get invested (For 25% off use my link below): https://t.co/19rezEdwTJ

Benjamin - Systematic... @Benjamin1524928

551 Followers 52 Following Traded discretionary for about 15 years and worked as a Data Scientist for 8 years before I decided to fully automate and go full time

S2N Navigator @S2N_Navigator

29 Followers 196 Following A backtesting & live trading platform with bias awareness & guardrails for humans and AI Agents. Newsletter: https://t.co/l8R0biE68E

m218714 @m218714

416 Followers 267 Following Some CS and finance experience | experimenting with systematic

Yuriy Matso @yuriymatso

78K Followers 372 Following Futures and equities algo trader. My strategies are here: 1) https://t.co/wkKGkCvKa2 and 2) https://t.co/SUi7ktYQnR

Kristjan Kullamägi �... @Qullamaggie

173K Followers 72 Following Traded $3K into $100M. Featured in the upcoming Market Wizards book. Live streamed my journey https://t.co/JsLb4klZoM Nowadays mostly lurking.

Pedro Silva @pedrosilva_net

1K Followers 164 Following Systematic trading, Mean Reversion and Momentum. You miss 100% of the ideas you don't backtest. Thinking in probabilities, trading with discipline.

Jeff Sun, CFTe @jfsrev

47K Followers 198 Following 16 years of stop losses, pain & grit to $ 10M multi-asset. My 17-Chapter Trader’s Guide - https://t.co/0F5tgGM49z

stevendu @Steven1_994

79K Followers 96 Following Day Trader| Mentor| Gamer| I turned $27k into 100M+ and I teach people to maximize their profits in the market with the most efficient strategies

Polymarket @Polymarket

1.6M Followers 6K Following The World's Largest Prediction Market. Trade politics, news, crypto, culture, sports, tech, & more. Discord: https://t.co/tzKrbDfF3x

DRYDEN @drydenwtbrown

28K Followers 5K Following STARTING A NEW COUNTRY LIVE @PRAXISNATION 🏳️ Escape the permanent underclass.

Quantifiable Edges @QuantifiablEdgs

21K Followers 132 Following Assessing Market Action with Indicators and History

Systematic Investment... @SystematicIRE

3K Followers 5K Following Systematic investor/trader, Kevin C Maki, PhD QV/MT investing = quality, value/momentum, trend Research scientist/educator, long-time investor/trader

ZenomTrader @ZenomTrader

11K Followers 323 Following Managing $4,900,000 in funded capital! 2-year verified track record! Sharing my growth! Private investor capital! AI/Tech/Inventor/Promethean!

elPythonQuantador @ThePythonQuant

14K Followers 668 Following Ex-Quant Trader. Unapologetically miserable. Views are my own.

Quantitative Finance ... @QFinancePapers

7K Followers 1 Following New Quantitative Finance papers from https://t.co/oAulCLLsgk. Thank you to arXiv for use of its open access interoperability.

Michael Melissinos @mmelissinos

2K Followers 10 Following Trend-Following. Founder of Melissinos Trading. Blog at https://t.co/vljIIOsKxn

Brandon @amphtrading

9K Followers 247 Following Full Time Trader | “Trusted Pine Programmer” endorsed by TradingView | MarketLens

Tivadar Danka @TivadarDanka

92K Followers 527 Following I make math and machine learning accessible to everyone. Mathematician with an INTJ personality. Chaotic good.

hughesanalytics @hughesanalytics

4K Followers 2K Following Systematic Long/Short Equity US S&P100. Financial Machine Learning. Quant trader.

Quanta Magazine @QuantaMagazine

362K Followers 615 Following Illuminating math and science. Supported by @SimonsFdn. 2022 Pulitzer Prize in Explanatory Reporting.

Caltropia Research @CaltropiaRes

316 Followers 163 Following Robust Quant Models and Investment Strategies for High Total and Risk Adjusted Returns

Ed Bradford @Fullcarry

54K Followers 453 Following US government bond trader since '93 with the usual stints along the way at primary dealers and HFs. Now on my own. Pseudonym

Kantro @MichaelKantro

111K Followers 947 Following Chief Investment Strategist @Piper_Sandler. Voted Wall Street's #1 Portfolio Strategist in '24 & '25. #HOPE. CFA. Girl dad. https://t.co/EBG0jU7WoE

Tom Dante @Trader_Dante

458K Followers 0 Following FX, Rates, Equities & Commodities Trader | 25 years in the markets | Creating consistently profitable traders

Tier1 Alpha @t1alpha

50K Followers 817 Following Leveraging Market Structure through Options, Volatility, Passive flows, and Systematic Rebalancing. Research Distributed through @Hedgeye

Cem Karsan 🥐 @jam_croissant

219K Followers 2K Following Founder, Kai Wealth. 27y Quant/Vol/Flow/Macro PM. Ex-MMaker,+10% of SPXOpt’s‘06-10 @phillipsacademy, @RiceAlumni,@KelloggAlumni, Vanna-Charmer🐍,🚫Invest Advice

Bob Elliott @BobEUnlimited

243K Followers 790 Following CIO at @UnlimitedFnds | PM of $HFGM, $HFEQ, $HFMF, $HFND | Fmr @Bridgewater IC | One of the few "sane" voices on #fintwit | Comments not investment advice

Jungle Rock @JungleRockRes

191K Followers 3 Following Jungle Rock is a systematic investment research and technology company. It runs a fintech platform for all market participants. @JungleRockCap 🇰🇾🇬🇧🇺🇸

Quan Duong @quandapro

929 Followers 68 Following Founder & CEO @ QNavix | Building QNavix | Algo Trader managing investor capital | Not financial

FX Physics @FXPhysics

767 Followers 6 Following 20+ year combined third-party audits by FundSeeder (RQSI), MarketLog, Darwinex Zero, Collective2 and Myfxbook: https://t.co/11xyv2b9V4

Quantifiable Alpha @QuantifiableA

477 Followers 218 Following Quantifiable Alpha: Exploiting market inefficiencies for quantifiable alpha. Crypto | Stocks | ETFs

Gappy (Giuseppe Paleo... @__paleologo

54K Followers 533 Following Gen Z boy in a Gen X body. Pronounciation: Jew ZEP peh (NOT pay!) Pah lay AW! low go. Sister account: @yogappygappy.

madaz @madaznfootballr

98K Followers 372 Following Full Time 8-Figure #Stonks Day Trader 🤑 w/15 Yrs Exp📈 #2 Ranked All Time Trader🏆(93.03% Career Win Rate) on @kinfo 📧:[email protected] IG:madazlifestyle

small_caps_automated @SmallCapSmarts

11K Followers 435 Following Algos, tools and research. Not selling any services, be cautious of potential scams.

Lone Wolf Trader @LoneWolfeTrader

3K Followers 40 Following Day trader and short seller. Strategy: $14k max per position, 100% stop loss. Monthly pnl posted via Kinfo includes locate costs and commissions.

Mallik @RealTQQQTrader

7K Followers 85 Following TQQQ/SQQQ systematic trader, Verified Trading track record at https://t.co/PrCM4RmTKn. Tweets are not financial advise.

Merritt Black @merrittblack

19K Followers 94 Following Founder, Head of Trading for @ApterosTrading. Ex Head of Futures for SMB Capital. Context is king.

Chris™ @ProbableChris

7K Followers 133 Following I trade $NQ using statistical models, probabilistic frameworks, and custom tools built based on my market perspective. Creator of @NQStats

Jim Carroll @vixologist

30K Followers 5K Following Portfolio manager with momentum and vol strategies. Also hack guitar player who sings. Tweets/RTs are not investment advice. You need to do your own work!!

Benn Eifert 🥷🏴�... @bennpeifert

120K Followers 1K Following Hedge fund manager (volatility/derivatives), QVR. Personal account. Oathbreaker paladin and Nightreign princess bodyguard. Chief Investment Officer of Antifa.Trends for United States

You might like